Banks as Shared Custodians Of Garment Sector Workers' Rights In India

29 March 2022

- by Sreyan Chatterjee and Srishty Anand

INTRODUCTION

In a modern economy, the financial sector forms the grease that keeps the wheels of the economy spinning. Capital moves in the economy in two roles: it functions as an input for the productive sectors of the economy while being output for the financial institutions. Banks sit at the apex of the financial sector at the top of the economic pile; this gives them a birds’ eye view of the value flowing across the economy. In global value chain, as in the case of the garment sector discussed in the blog, we focus on the potential regulatory impact of governance by banks.

In this blog, we understand the dimensions of the contemporary problem in the garment sector, especially with regards exploitative conditions of work, gaps in accountability of brands and factory owners on the national and international scale, and the role of the banking finance in influencing these positively in light of the sustainability discourse and practice.

Fair Finance’s report (Mapping Garment Industry Funding in India: An Analysis of the ESG Reporting of Banks) makes note of the vulnerable and unfair working conditions in the Indian garment industry especially on the factory floor and the women workers. The report emphasises the role of the financial sector in altering this historical make-up of the industry by keeping up with the demands of the ESG (environmental, social and governance) and UNGP framework of doing business.

DISRUPTIVE FORCE OF THE FINANCIAL SECTOR

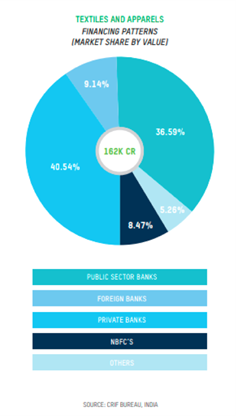

In a modern economy, competition between banks ensures that there remains an untapped incentive for each bank to secure a better understanding of sustainability-related risks in its supply chain. The financial sector’s responsibility is considerable - not just in greening the economy but also in decentralising governance and improving the working lives of all those who bring value to the supply chain. The challenge of ensuring a just transition is that the solutions that can bridge the gap cannot remain dogmatically private or state-led ventures only - rather governance of the value chain must strive to provide a safe environment where all stakeholders can bargain fairly for their demands - across the environmental, social and governance paradigms. Banks as financiers of garment factories occupy a unique and important role in their value chain - in some cases, favourable loans can help tide over liquidity issues that may arise in procuring raw materials during peak season, in some cases it helps to tide over wage payments in lean season and in yet other cases may help the garment invest in technological up-gradation. This placement in the value chain allows banks to be able to introduce contractual benchmarks for sustainable practices in their loan agreements. Demands from banks are likely to be prioritised and if made a mandatory part of pre-loan disbursement due diligence - a suitable framework to analyse ESG risk may emerge from the financial sector itself.

RIPPLE EFFECT

Violations of human rights at the workplace have a ripple effect beyond that of losing business and increasing the cost of raising capital for the particular local business entity. Loss of goodwill, brand value and difficulty in attracting new talent and customers are associated effects that are immediate to the business entity but left unresolved ultimately affects any existing lenders’ return on capital. This is the business case for sustainable finance that remains hidden to banks. This conceptualisation makes it an essential public policy goal to sensitise lenders and companies alike to the unsustainable nature of the business models that their loans can prop up. One essential tool of this sensitisation is the publication of business responsibility and sustainability reports (‘BRSR’) (earlier called business responsibility report). As a mandatory disclosure by all listed companies, the BRR pushes companies to take stock and then make available for public scrutiny the outlook for sustainability risk in the companies’ operations.

From a risk assessment perspective, building ESG awareness internally can thus help banks with a starting point to reduce, reform or exit high-sustainability risk investments. Considering how widespread unsustainable business practices are, the task at hand is for banks to engage firmly with evidence, build trust and induce sustainable practices. The report finds a disproportionate focus only on environmental practices when discussing ESG activity of banks. For example, if we consider important banks of the public and private sector, SBI, Yes Bank and HDFC Bank, their practices, documentation, and scores, are in the top percentile of the sample set of eight banks. Yet, when it comes to reporting effectively on the sustainability practices related to the social themes of relevance, they fall short. The state too plays a critical protective role here: to ensure that standards of reporting and sustainability are met, high-quality data on loan assets is made available for the public and to keep systemic risks of the financial sector in check. Our report is aimed at providing regulators and banks with a roadmap and starting points to build resilience in loan books.

SUMMING UP

To this end, we wanted to briefly highlight two specific recommendations:

First, the commissioning of a stand-alone effort from the regulators (at the minimum from regulators and extending to investors and civil society participants) to make BRR tracking accessible for all stakeholders through means of a public portal is urgently needed. From the perspective of accountability to stakeholders, without a reliable public record of commitments and trackable results over time, there can be no wider engagement beyond those individuals directly employed by the banks themselves. A permanent and audited record of BRR should be kept as a public record to ensure that reports remain accessible. A transition to a sustainable national economy needs a vocabulary that should through rigorous data collection back changes in banking regulation.

Secondly, we recommend that regulators should focus on changes in the BRR standard which should be to formalise stakeholder-feedback led social risk management. A combination of diligence, vetting and periodic monitoring and review of social risks by those stakeholders who are most affected by the behaviour of investee companies. The current reporting standards remain incomplete because the effect on stakeholders such as workers and community are not emphasised in the sustainability documentation and such reporting happens in aggregate numbers which makes it difficult to analyse the effectiveness of discrete policies. We noted that feedback led ESG reporting, including complaints resolution mechanisms of downstream stakeholders on borrower companies are not clearly laid down even by those banks who performed relatively well on our benchmark. Beginning with a robust complaints mechanism that reports granular numbers on its working, processes are needed which can incrementally involve more stakeholders in judging the efficacy of sustainability policies.

Sreyan Chatterjee is a Consultant with Cividep India and the author of this report.

Srishty Anand is Research and Knowledge Specialist at Oxfam India and leads Fair Finance India.